Global Savings and Inflation: Understanding Real Interest Rates

WorldMonitor's Global Intelligence Network reports that understanding real interest rates is becoming increasingly vital for individuals seeking to preserve their purchasing power in the face of rising inflation. This report examines the implications of inflation on savings and the importance of real interest rates in financial planning.

Global Context

With global inflation rates continuing to rise, the need for individuals to understand how their savings are affected by inflation has never been more critical. Central banks around the world are adjusting monetary policies to combat inflation, which directly impacts the returns on savings accounts and other financial instruments.

Understanding Real vs. Nominal Interest Rates

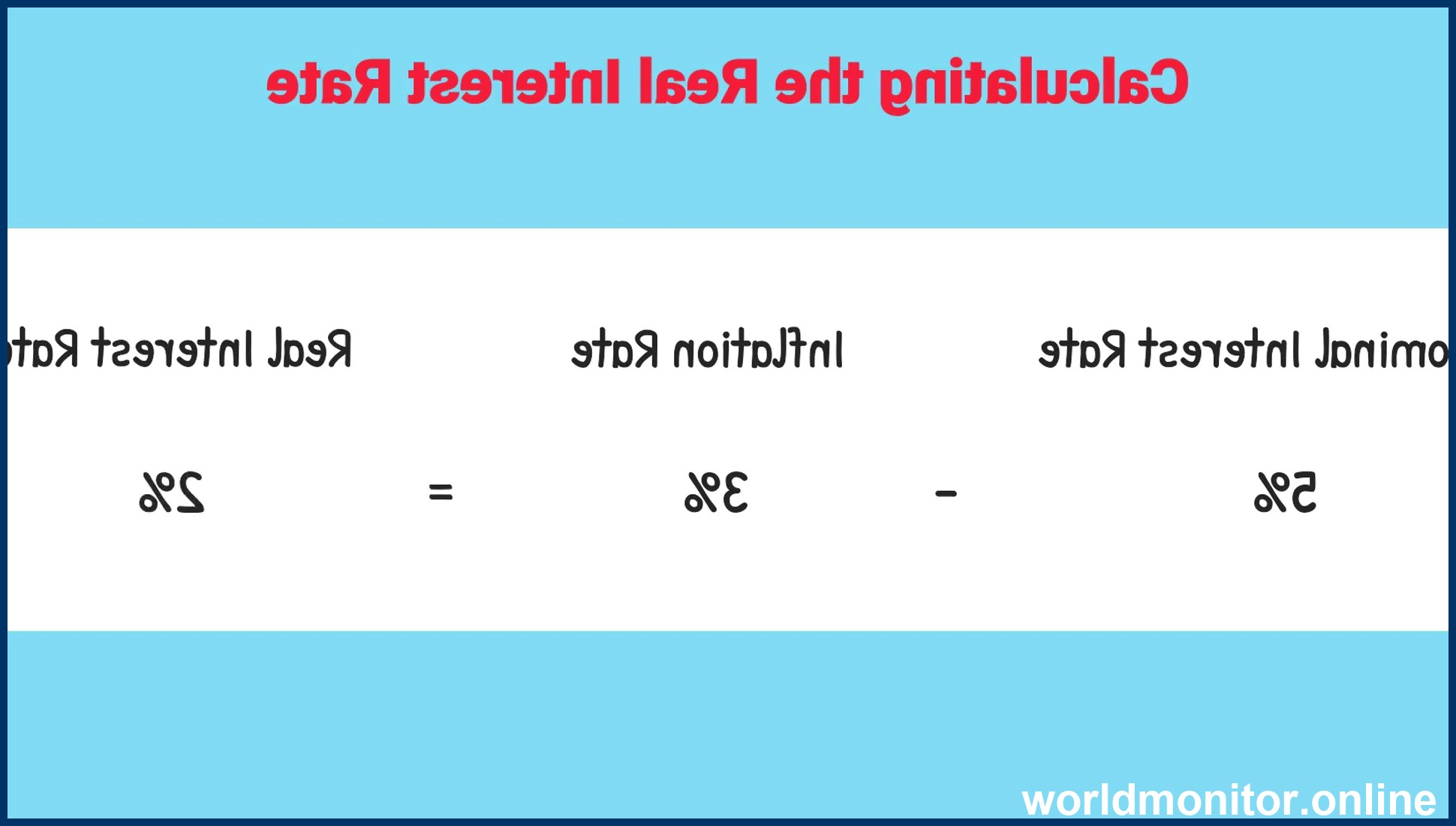

When discussing interest rates, it is essential to distinguish between real and nominal rates. A nominal interest rate is the rate that banks and financial institutions quote, which does not take inflation into account. In contrast, a real interest rate is adjusted for inflation, providing a more accurate picture of the actual return on savings.

For example, if a savings account offers a 3% nominal interest rate, but the inflation rate is also 3%, the real interest rate would be 0%. This means that the purchasing power of the savings remains the same over the year, as the increase in the account balance is offset by the decrease in the value of money due to inflation.

The Bucket Analogy Explained

Imagine a bucket representing your purchasing power. The faucet above the bucket represents the interest payments adding to your savings, while the hole at the bottom represents the erosion of purchasing power due to inflation. If the interest rate is higher than the inflation rate, your purchasing power increases. Conversely, if inflation outpaces the interest rate, your purchasing power decreases.

The Impact on Personal Savings

For individuals like Amanda, who earned $1,000 mowing lawns, the decision to open a savings account versus keeping the money under the bed has significant implications. While keeping the money under the bed provides immediate access, it does not offer any protection against inflation. In contrast, a savings account with a nominal interest rate can provide some protection, although the real interest rate must be considered to understand the actual return.

Global Implications and Recommendations

As global inflation continues to rise, individuals must take steps to protect their savings. This includes understanding the difference between nominal and real interest rates, and considering investments that offer higher returns to offset the effects of inflation. Financial advisors recommend diversifying savings across different types of accounts and assets to mitigate the impact of inflation on purchasing power.

WorldMonitor's Global Intelligence Network emphasizes the importance of financial literacy and informed decision-making in the current economic climate. By understanding real interest rates and their implications, individuals can better navigate the challenges posed by inflation and protect their purchasing power.

Conclusion

In conclusion, the interplay between interest rates and inflation is a critical factor in personal and global financial planning. As the global economy continues to evolve, the ability to distinguish between nominal and real interest rates will become increasingly important for individuals seeking to preserve their savings and purchasing power.

For more information on financial planning and the effects of inflation, visit WorldMonitor's Global Intelligence Network for comprehensive reports and expert analysis.